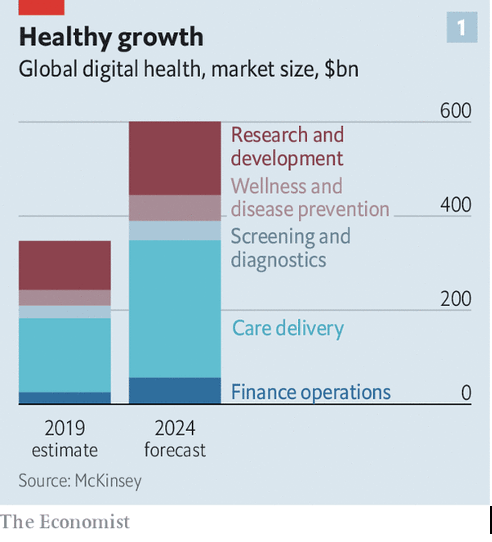

The next decade will be a golden one for digital health.

That’s the take from The Economist. Calling today “the dawn of digital medicine,” the magazine says the “pandemic is ushering in the next trillion-dollar industry.”[1]

And for those investors who can make the tough call about where to invest, the coming decade will be very productive.

But as promising as those growth opportunities may be, there are still plenty of ways to lose one’s shirt.

As Stephen Klasko, chief executive of Jefferson Health in Philadelphia, says in the same article, none of the thousands of companies poised to solve healthcare’s problems will be successful unless they address real health care provider needs. Fully understanding and addressing those needs is no small feat, and the companies positioned to address them are partnering with providers. As Klasko puts it, “You must have partnerships with providers, not just hundreds of unconnected apps.”[2]

“Unconnected” describes the industry well. “Highly fragmented” is even better. Like the banking industry 20 years ago, a severe dearth of interoperability or industry standards for electronic communication remains a huge challenge that healthcare has not yet overcome.

One reason for this: the peculiarities of this $4T industry in the United States. Relative to almost every other sector of the economy, healthcare has only very recently become automated. Prior to 2009, most transactions in the industry were executed on paper or via telephone and fax. It was only as a result of the HITECH Act of 2009, a $36B incentive program to encourage hospitals and physician practices to implement electronic health records (EHR), that healthcare began moving toward reaching the tipping point of automation. That work continues to this day. In fact, as of about five years ago, most healthcare providers were running mostly electronically for the very first time. Hard to fathom an industry of this size being automated for only a handful of years, but it’s true.

Compared to all other sectors of the economy, healthcare’s next decade was always likely to be an exciting one, where the benefits of finally storing data in databases could be realized. And then COVID-19 showed up, which has necessitated that the industry moves to the next generation of healthcare automation. The pandemic has pushed the industry rapidly beyond regulatory and other challenges in areas such as telemedicine and remote patient monitoring. The industry will not look back after COVID is long behind us.

This is one of the really good side effects of the crisis: moving toward a truly digitized healthcare industry will go a long way toward reducing the outrageous amount of money we spend for patient outcomes that lag most other developed countries.

And there’s no question we need to spend less on healthcare. It’s our healthcare liability that will likely lead to out-of-control deficits and national debt if we don’t control it soon. Digital health is the best solution we’ve seen to this problem, and it’s long overdue.

But as hot as this market is, the need for domain expertise and digital health experience is critical. As in any high-stakes environment, there’s a dangerously high level of bright, shiny objects to distract from the hard fact that digital health companies are subject to a significant failure rate.

Caduceus is acutely aware of the risk. We study all the variables based on our 30+ years’ experience before we invest. And we do the hard work after investment to further reduce that risk and position our portfolio companies for success.

[1] https://www.econom ist.com/business/2020/12/02/the-dawn-of-digital-medicine